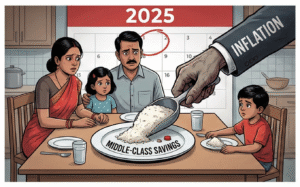

How Inflation Is Affecting Middle-Class Savings in India: The Silent Financial Crisis of 2025

The Indian middle class has always been known as the backbone of the nation’s economy—earning, saving, investing, educating children, buying homes, and paying taxes on time. But in 2025, something dangerous and silent is happening. Inflation is slowly eating into middle-class savings, and millions of families are feeling financially weaker despite earning more than ever before.

Groceries cost more, school fees rise every year, medical expenses jump without warning, fuel prices fluctuate wildly, and EMIs never seem to go down. Yet salaries grow slowly. The result? Savings are shrinking, investments are delayed, and financial anxiety is rising.

This blog explains—in simple language—how inflation is affecting middle-class savings in India, why it feels harder to save today, what numbers you must understand, and what practical steps you can take to protect your future.

✅ What Is Inflation and Why It Matters So Much to the Middle Class

Inflation simply means a rise in prices of goods and services over time. When inflation increases, the purchasing power of your money falls. In simple terms:

What you could buy for ₹100 last year may cost ₹110–₹120 today.

For the middle class, inflation is especially dangerous because:

- Income growth is fixed or slow

- Expenses are rigid and unavoidable

- Lifestyle costs constantly increase

- There is no free subsidy cushion

- Savings are expected to fund retirement, children’s education, and healthcare

✅ Inflation in India: The 2025 Reality

India’s inflation in recent years has been driven by:

- Food inflation (vegetables, pulses, grains)

- Fuel and LPG price fluctuations

- Rising healthcare and insurance costs

- Education fee inflation

- Rent and housing maintenance

- Imported inflation due to global disruptions

Even when official inflation numbers appear moderate, the real household inflation faced by the middle class often feels much higher—sometimes 9% to 12% annually.

This means if your money grows at 5–6% but your expense inflation is 10%, you are actually becoming poorer in real terms.

✅ How Inflation Is Destroying Middle-Class Savings — Step by Step

Let’s break down this silent financial damage in real-life terms.

✅ 1. Grocery Bills Are Rising Faster Than Income

Five years ago, a middle-class family spent ₹6,000–₹8,000 per month on groceries. In 2025, that number easily crosses ₹12,000–₹15,000.

- Milk, curd, vegetables

- Cooking oil, wheat, rice

- Fruits and packaged food

Each item shows a small monthly rise, but together they crush savings.

📉 Result:

Money that earlier went into RD, SIP, PPF is now going into daily survival.

✅ 2. Education Costs Are Becoming a Savings Killer

School and college fees are increasing at 10–15% annually in many cities. Add to that:

- Coaching classes

- Online learning platforms

- Devices, books, transport

For families with two children, education alone eats up 30–40% of income.

📉 Result:

Parents sacrifice:

- Retirement savings

- Mutual fund investments

- Emergency funds

✅ 3. Medical Inflation Is the Biggest Fear

Medical inflation in India is estimated at 12–14% annually, much higher than normal inflation.

- Hospitalization

- Diagnostics

- Long-term medication

- Health insurance premium hikes

A single hospitalization can wipe out 5–10 years of savings.

📉 Result:

Middle-class families are forced to:

- Break FDs

- Withdraw mutual funds early

- Take personal loans

✅ 4. EMI + Inflation = Financial Suffocation

Home loan EMIs, car loans, education loans—all rise when interest rates increase. At the same time, daily expenses rise due to inflation.

✅ Fixed income

✅ Rising EMI

✅ Rising living cost

This triple pressure leaves almost nothing for savings.

📉 Result:

Savings rate falls sharply after buying a house or car.

✅ 5. Lifestyle Inflation Is Also a Silent Enemy

As income rises slightly, lifestyle expenses rise automatically:

- Better mobile phones

- OTT subscriptions

- Eating out

- Weekend travel

- Branded clothing

These are not luxuries anymore—they are seen as “normal lifestyle.” But they drain savings slowly.

📉 Result:

You feel richer temporarily but become weaker financially.

✅ The Shocking Truth: Middle-Class Savings Rate Is Falling

Earlier, a typical Indian middle-class household saved 25–30% of income. In 2025, this number often drops to:

- 10–15%

- Sometimes 0%

- Sometimes negative (debt-driven lifestyle)

This is alarming because:

- Retirement is fully self-funded now

- Pension systems are weak

- Medical costs rise sharply with age

✅ Inflation vs Salary Growth: A Losing Battle

For most salaried employees:

- Average annual salary increment = 6–8%

- Real household inflation = 9–12%

This means:

Even if your salary increases every year, your real wealth is declining.

That is why:

- You feel financially stuck

- Savings don’t grow

- Wealth creation feels impossible

- Retirement feels uncertain

✅ How Inflation Is Affecting Different Types of Middle-Class Savers

🔹 1. Salaried Employees

- Tax burden + inflation = double attack

- Limited scope for side income

- Fixed increments

- EMI pressure highest

🔹 2. Small Business Owners & Self-Employed

- Revenue fluctuates but costs keep rising

- Raw material inflation

- Rent and electricity hikes

- Unstable savings

🔹 3. Young Professionals

- Late savings start

- Higher lifestyle spending

- Heavy education loans

- Peer pressure consumption

🔹 4. Retired Middle Class

- Pension loses real value

- FD returns fail to beat inflation

- Health costs explode

- Children’s dependence continues

✅ Why Traditional Saving Methods Are Failing Against Inflation

❌ Fixed Deposits (FD)

Average FD return: 6–7%

But real inflation: 9–10%

➡️ Real return = Negative

❌ Recurring Deposits (RD)

Returns barely beat FD. They no longer protect purchasing power.

❌ Savings Account

At 3–4% interest, money actually loses value year after year.

✅ Only Asset Classes That Can Fight Inflation

- Equity Mutual Funds

- Direct Stock Investments

- Real Estate (selectively)

- Gold (partial hedge)

- REITs & Index Funds

✅ Emotional Impact of Inflation on the Middle Class

Inflation doesn’t just affect money—it affects:

- Mental peace

- Family happiness

- Marriage decisions

- Child planning

- Career risks

- Health choices

People now:

- Delay buying homes

- Avoid having second child

- Postpone retirement

- Work beyond 60

✅ Real-Life Example: The Shrinking Middle-Class Dream

A family earning ₹10 lakh per year in 2010 lived comfortably. In 2025, even ₹15–18 lakh per year often feels tight due to:

- School fees

- Home EMI

- Healthcare

- Transport

- Taxes

- Inflation on essentials

Savings that once funded:

- Property

- Business

- Retirement

Now only manage:

- Emergency survival

✅ What Middle-Class Indians Can Do to Beat Inflation

✅ 1. Shift from “Saving” to “Investing”

Saving alone won’t work anymore. You need:

- SIPs in equity funds

- Index funds

- Balanced advantage funds

✅ 2. Increase Income, Not Just Cut Expenses

- Side hustles

- Freelancing

- Digital skills

- Online business

- Consulting

✅ 3. Prepay High-Interest Loans

Credit cards, personal loans, and long EMI tenures are inflation disasters.

✅ 4. Health Insurance Is Non-Negotiable

A single hospital bill can destroy decades of savings.

✅ 5. Track Your “Real Savings Rate”

Calculate:

Income – (All Expenses + Hidden Inflation)

This gives your true financial progress.

✅ The Role of Government and RBI in Inflation Control

- RBI controls inflation through interest rates

- Government controls through:

- Subsidies

- Tax policies

- Food stock management

- Fuel pricing strategies

But policy-level control always takes time. Meanwhile, the middle class absorbs the shock first.

✅ Is the Middle Class Shrinking in India?

Economically, yes.

Many families are:

- Moving from middle class → lower-middle class

- Struggling to upgrade lifestyle

- Unable to accumulate assets

- Getting trapped in EMI cycles

The “new middle class” is earning more but saving less than ever before.

✅ Future Outlook: What Will Happen If Inflation Stays High?

If inflation remains elevated for the next 5–10 years:

- Retirement crisis will deepen

- Housing affordability will worsen

- Education will become more exclusive

- Wealth gap will widen

- Financial stress-related health issues will rise

✅ Final Verdict: Inflation Is the Biggest Enemy of the Indian Middle Class

Inflation is not just a number announced by economists. It is:

- Your shrinking savings

- Your rising EMI

- Your delayed retirement

- Your increasing medical risk

- Your vanishing financial safety

The middle class today is working harder than ever—but saving less than ever.

If you don’t actively fight inflation, inflation will silently destroy your financial future

✅ Conclusion

The Indian middle class does not need sympathy—it needs financial awareness, strategic investing, disciplined planning, and income expansion. Inflation will not wait for anyone. The ones who adapt early will survive with dignity. The ones who ignore it will struggle silently.

Your future wealth depends not on how much you earn—but how well you protect your money from inflation.

For More Such Amazing Content Please Visit : https://investrupeya.insightsphere.in/

Post Comment