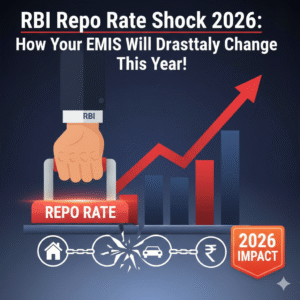

Impact of RBI Repo Rate on Home Loan EMI in 2025: What Every Borrower Must Know

In 2025, lakhs of Indian families are struggling to balance their monthly budgets due to rising living costs, taxation changes, and most importantly—fluctuating home loan EMIs. At the heart of these EMI changes lies one powerful financial tool controlled by the Reserve Bank of India (RBI): the Repo Rate.

Many borrowers hear this term often in news headlines but fail to understand how the RBI repo rate directly impacts their home loan EMI. This blog explains everything in simple language—from what repo rate is, how it affects banks, how your EMI changes in 2025, and how you can protect your finances from future rate hikes.

✅ What Is RBI Repo Rate?

The Repo Rate is the interest rate at which the Reserve Bank of India lends money to commercial banks for short-term needs. It acts as a control lever for the entire economy.

- When RBI increases repo rate → Loans become expensive

- When RBI cuts repo rate → Loans become cheaper

Since most home loans in India are now linked to floating interest rates based on repo rate, even a small change directly affects your EMI.

✅ Why RBI Changes Repo Rate in 2025

In 2025, RBI continues to adjust repo rates mainly due to:

- Inflation control

- Fuel and commodity price volatility

- Global interest rate movements

- Economic growth protection

- Currency stability

If inflation rises sharply, RBI increases repo rate to slow down spending. If the economy slows down, RBI reduces repo rate to encourage borrowing and investment.

✅ How Repo Rate Affects Home Loan EMI

Let’s understand the direct relationship between repo rate and your EMI:

When repo rate increases:

- Banks increase their lending rates

- Home loan interest rates rise

- Your EMI increases

- Total interest paid over loan tenure increases

When repo rate decreases:

- Banks reduce loan rates

- EMI decreases

- Borrowers save interest

- Purchasing power increases

✅ Example: How EMI Changes Due to Repo Rate in 2025

Let’s assume:

- Loan Amount = ₹50 lakh

- Tenure = 20 years

- Earlier Interest Rate = 8.5%

- New Interest Rate after hike = 9.25%

EMI Impact:

- EMI at 8.5% ≈ ₹43,391

- EMI at 9.25% ≈ ₹45,927

✅ EMI increases by ₹2,536 per month

✅ Extra burden per year = ₹30,432

✅ Extra interest over 20 years = ₹6–8 lakh approx

This clearly shows how risky frequent repo rate hikes can be for long-term borrowers.

✅ Home Loan Trends in 2025

The housing finance market in 2025 is witnessing:

- Higher floating rate loans

- Fewer fixed-rate options

- Increased co-lending models

- Faster repo-linked rate transmission

- More digital refinancing platforms

This means borrowers now feel EMI changes much faster than in previous years.

✅ Who Is Most Affected in 2025?

The biggest impact is felt by:

- Middle-class salaried employees

- First-time home buyers

- Self-employed professionals

- Young couples with new housing loans

- People under 30-year loan tenure

For them, even a ₹1,500–₹3,000 EMI hike disrupts savings, SIPs, insurance and emergency funds.

✅ Fixed vs Floating Home Loans in 2025

| Fixed Rate Loan | Floating Rate Loan |

| EMI remains same | EMI changes with repo rate |

| Higher interest initially | Lower interest initially |

| No benefit of future cuts | Full benefit of rate cuts |

| Suitable for short tenure | Better for long-term loans |

🔍 In 2025, most banks prefer floating rate loans, transferring rate risk directly to borrowers.

✅ Benefits When Repo Rate Falls

If RBI cuts repo rate in 2025, borrowers enjoy:

- Lower EMI burden

- Faster loan repayment

- Increased monthly savings

- Better financial breathing space

- Improved credit demand in housing

This also leads to real estate demand growth, builder confidence rise and job creation.

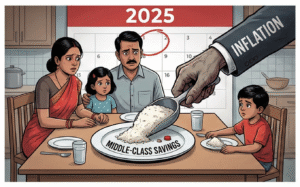

✅ Risks of Continuous Repo Rate Hike

- Long-term interest cost increases sharply

- Housing affordability drops

- Default risk rises

- Middle-class savings decline

- Consumer confidence weakens

Higher EMIs can turn a good loan into a financial trap if not managed properly.

✅ How to Protect Yourself from EMI Shock in 2025

Here are smart borrower strategies:

✅ 1. Increase EMI Instead of Tenure

Do not extend loan tenure during hikes. Pay slightly higher EMI to reduce interest burden.

✅ 2. Prepay Whenever Possible

Annual bonus, tax refunds, or savings can be used to prepay principal.

✅ 3. Refinance Your Loan

Check offers from other banks with lower spreads over repo rate.

✅ 4. Maintain Emergency Fund

Keep at least 6 months of EMI + expenses in liquid savings.

✅ 5. Avoid Top-Up Loans in High-Rate Periods

Top-up loans attract higher floating interest rates.

✅ Impact on New Home Buyers in 2025

For new home buyers:

- Loan eligibility reduces

- Down payment requirement increases

- Property affordability declines

- Project delays become costly

- EMI-to-income ratio worsens

Banks now ensure EMI does not exceed 40–45% of monthly income, making approvals stricter.

✅ RBI Repo Rate vs Inflation in 2025

In 2025, RBI is walking a tightrope between:

- Controlling inflation

- Supporting growth

- Maintaining liquidity

- Protecting currency

If inflation stays high, repo rate will remain tight. This means home loan EMIs may stay elevated longer than expected.

✅ Is This a Good Time to Buy a House in 2025?

It depends on your financial stability:

✅ Buy Now If:

- You have stable income

- You have 30–40% down payment

- EMI fits easily into budget

- Property is end-use, not investment

❌ Wait If:

- Income is uncertain

- You’re stretching EMI limits

- Loan tenure is above 25 years

- You depend on future rate cuts

✅ What Experts Predict About Repo Rate in 2025

Most market analysts believe:

- Repo rates will remain range-bound

- Sharp cuts are unlikely unless inflation softens

- Floating-rate loan pressure may continue

- Housing demand will remain cautious but stable

✅ Key Takeaways for Home Loan Borrowers

✔ Repo Rate directly controls your EMI

✔ Floating loans are highly sensitive

✔ Even 0.5% hike can cost lakhs

✔ Proper prepayment strategy is essential

✔ Financial discipline matters more than ever in 2025

✅ Final Verdict

The impact of RBI repo rate on home loan EMI in 2025 is powerful, immediate, and unavoidable. With inflation uncertainties and global financial pressures, borrowers must remain alert. Blindly assuming that EMIs will always remain affordable is a dangerous mistake.

If you already have a home loan, start planning your prepayment and EMR management strategy today. If you’re planning to buy a house in 2025, calculate your worst-case EMI scenario before signing any loan agreement.

A home loan should build your future—not burden it.

For More Such Amazing Content Please Visit : https://investrupeya.insightsphere.in/

Post Comment